If you are an SME owner thinking about selling your business or bringing in a strategic partner, the first thing that probably comes into your mind is “So…how much can I sell it for?” It is totally a fair question, but in mergers and acquisitions (M&A), the “price” does not come from a number casually pulled from an Excel sheet or a quick online calculator.

Valuation is based on a structured set of methods that estimate what a business is truly worth, and just as importantly, what a buyer is realistically willing to pay. These methods consider factors such as the company’s ability to generate earnings and cash flow, its risks profile, growth potential, and how confident a buyer feels about the business continuing to perform after the deal.

And here is the key point many owners tend to overlook – valuation is not just about “getting a price.” It influences the entire deal journey, like how buyers respond, what terms they propose, whether earn-outs are required, and how strong your negotiating position ultimately is. A well-thought-through valuation helps sellers understand what their business truly worth, while also setting a number that buyers can reasonably accept.

This is especially important for SMEs, where financial reporting may be less standardized and the business may rely heavily on founders or a small group of key customers. In these situations, valuations become more sensitive and even more important to get it right. When done properly, it creates a solid foundation for constructive discussions.

The Three Main Valuation Methods Used in M&A

In practice, the best M&A valuations rarely rely on just one method. Instead, using a combination of approaches gives a more balanced view of what is fair and reasonable for the deal. This is why advisors often present a valuation range, as it reflects different situations and gives both sides room to discuss what could shift value up or down.

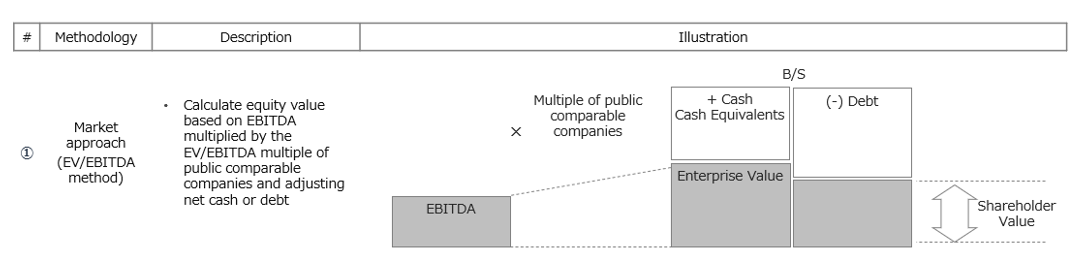

1. Market Approach (e.g. EV/EBITDA method)

The market approach is commonly expressed using the EV/EBITDA method. It values a business by applying a market multiple to its earnings, based on how similar businesses are priced. Its basic logic is “Companies like yours trade at around X times EBITDA, so your implied value is approximately EBITDA x Market multiple.”

EBITDA represents operating earnings, while Enterprise Value (EV) reflects the value of the entire business before debt and cash.

Formula in simpler view: EV = EBITDA x Market Multiple

Before applying a multiple, buyers usually want normalized EBITDA – meaning earnings adjusted to reflect the business’s true, ongoing performance. This matters especially for SMEs, where accounts may include items that will not continue after the sale, such as owner-related expenses or one-off costs.

Simple example:

If reported EBITDA is RM2 million, but normalization adjustments increase it to RM2.5 million, and comparable businesses trade at 5x to 7x EBITDA, the implied EV range would be RM12.5 million to RM17.5 million. After deducting RM3 million of net debt, the equity value range would be approximately RM9.5 million to RM14.5 million, before final deal adjustments.

This method is popular because it is easy to understand and benchmark. It works well for businesses with stable earnings and comparable peers, but it also involves judgment, particularly around EBITDA add-backs and the multiple that best reflects risk. In addition, EBITDA does not always reflect cash flow reality, as companies with similar EBITDA can have very different working capital or capex needs. Therefore, buyers often treat EV/EBITDA as a useful market reference rather than a standalone answer, and cross-check it against other valuation methods. In cross-border M&A, this is even more important, as market multiples vary by geography and what feels “normal” locally may look aggressive or conservative to overseas buyers, leading to deeper discussions on risk and growth assumptions.

2. Cost Approach (e.g. Net Asset Value method)

The cost approach looks at the company’s balance sheet rather than its earnings, or in an easier way to understand, it refers to “Total Assets – Total Liabilities”

This method is particularly relevant for asset-heavy companies such as real estate, logistics, oil & gas, manufacturing, and semiconductors, which often have substantial investments in tangible assets.

However, in many M&A deals, buyers will go one step further to reassess whether balance sheet figures reflect fair market value, especially when assets were acquired years ago.

Simple example:

If a company has RM10 million in assets and RM4 million in liabilities, net assets are RM6 million. If a property recorded at RM2 million is now worth RM5 million, adjusted assets become RM13 million, lifting net assets to RM9 million.

In cross-border transactions, the cost approach is often used as a sense check, particularly by overseas buyers who want reassurance that downside risk is supported by tangible assets. However, it may undervalue businesses where most value lies in earnings and intangibles, such as customer relationships, brand, systems, or know-how – which is why it is typically used alongside earnings-based methods.

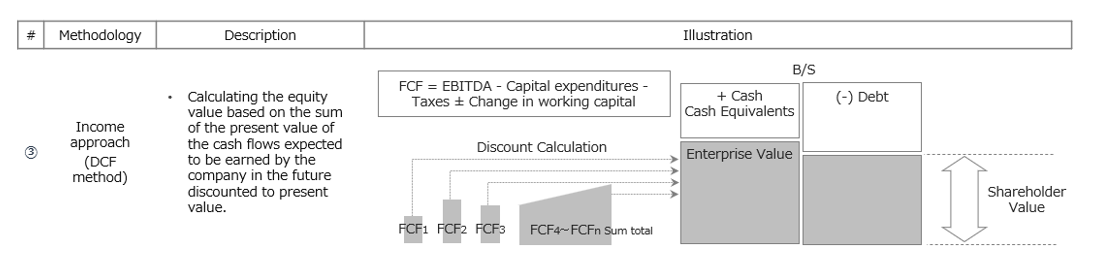

3. Income Approach (e.g. Discounted Cash Flow (“DCF”) method)

The DCF method estimates value based on the future free cash flow a business is expected to generate over the next 3 – 5 years, discounted back to today using a discounted rate that reflects risk. In simpler terms, it asks “If I buy this business today, what cash will it generate for me in the future, and what is that worth today?”

Simple example:

If a business is expected to generate RM1 million in free cash flow per year for the next 5 years, a buyer will not simple say, “That’s RM5 million.” Future cash carries risk and time value. Using, for example, a 15% discount rate, those cash flows are adjusted back to today’s value. Buyers typically also include a terminal value, representing the business’s value beyond year five.

DCF is powerful because it is fundamentals-driven and can reflect the specific dynamics of a business, such as expansion plans or cost improvements. It works best when cash flows are predictable and forecasts are credible.

When cross-border deal is involved, DCF is often used as a common valuation language when accounting standards, market benchmarks, or industry multiples differ across countries. Overseas buyers may rely more heavily on cash flow forecasts to understand how the business performs under different economic, regulatory, and even currency conditions. As a result, assumptions are often scrutinized more closely, making transparent and well-supported forecasts especially important for SMEs.

A clear understanding of the three main valuation methods helps bring the valuation conversation back to fundamentals. Each method provides a different lens on value, for example, future cash generation, market pricing of earnings, and balance-sheet support. This is why a reasonable valuation range is often the most defensible outcome, especially in cross-border M&A, where differences in expectations can otherwise slow or derail discussions.

Because valuation sits at the intersection of technical analysis and negotiation, having an experienced advisor can make a meaningful difference. In cross-border transactions, differences in market norms, valuation benchmarks, and risk perception often need to be carefully bridged. Nihon M&A Center Malaysia supports this process by conducting valuation work in-house, advising sellers on true value drivers that resonate with potential buyers, and translating business performance into a clear, buyer-ready narrative. Beyond the numbers, we also help manage discussion with the buyers, helping both parties align expectations, addressing differences in EBITDA normalization, fair value adjustments, and multiple assumptions, and move toward a realistic valuation that supports constructive negotiations.

Ultimately, valuation is not just a calculation. It is a structured process that manages expectations, supports decision-making, and reduces friction throughout the transaction journey. When prepared properly and guided professionally, valuation becomes less about arguing over “the right number,” and more about creating clarity that helps both parties move forward with confidence.

Considering a local or cross-border M&A transaction? Let our team help you navigate valuation, align expectations, and prepare for a smoother negotiation process.